How do I calculate the cost of complaints?

Do you need to get a rough idea of how much customer complaints are hurting you?

Use this formula when talking to your Chief Financial Officer to measure the bottom line impact from the complaints you are receiving. Market Research has also published a decent page on how your complaints are just representing the tip of the iceberg.

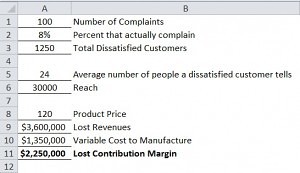

Received complaints represent a small percent of loss. The example below shows how just 100 complaints on a product that costs $120 equals over $2 million in lost profit potential.

Calculate the cost of complaints:

_______ Number of complaints

_/_.08__ Divide by 8%: average number that actually do complain – some estimates are as low as 4%

= _____ Total dissatisfied customers

x __24__ Average dissatisfied customer tells/influences 24 people, who probably won’t buy your product. Twenty four (24) seems to be the common number used on the internet, but none were backed up by citing an actual study. TARP was a common research outfit mentioned.

= __ ___ Reach

x $____ Multiply by the price of product

=_____ Total lost revenues

-_____ Subtract the variable cost to produce your product

=_____ Lost contribution to margin

Example

100 complaints on a product that costs $120 represents over $2 million in lost profits when you calculate the cost of complaints

This lost contribution margin can give you a rough idea of the potential budget for improving quality and handling customer complaints. It is only part of the total but it should get the conversation going with your CFO’s office. It’s difficult to put a dollar value on loss of brand value, potential punitive damages or the costs associated with regulatory warning letters (and the increased scrutiny that comes with them). Recreate the table here to calculate the cost of complaints.